In the world of global custody and securities services, scale isn't just an advantage, it's the ultimate bedrock of survival for service providers. Both major and mid-tier players have grown considerably in terms of Assets under Custody – the quantum of their client assets – over the past 25 years.

Since the year 2000, globalcustody.net has been the go-to resource for Assets under Custody and Administration data for the world's leading providers of securities services. The data tells a definitive story of strategic acquisitions and 'near-miss' mergers, a journey from the first USD 10 trillion milestone to a modern era defined by technological arms races and service strength and consistency.

Shifting Sands in the Mid-Tier

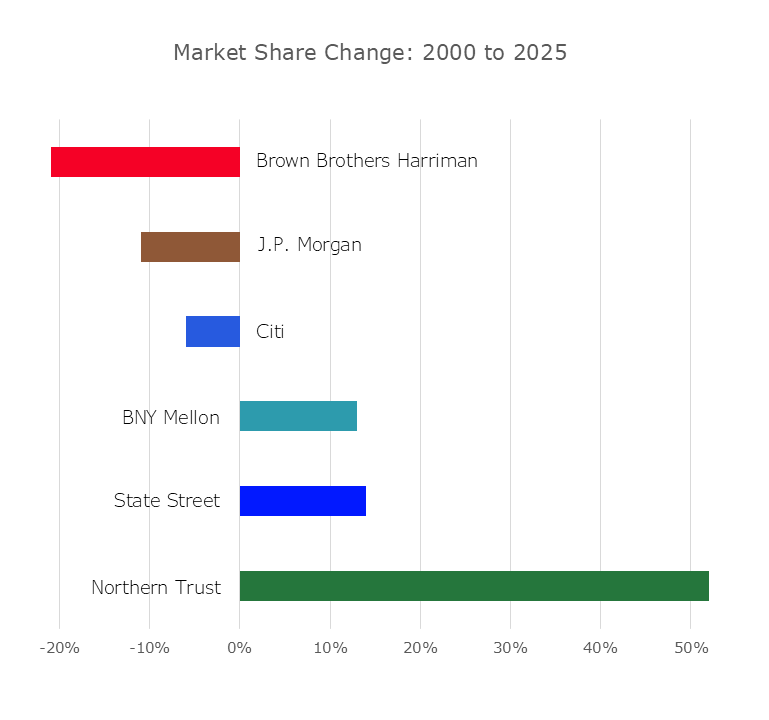

While the dominance of the mega-custodians is undeniable, their collective market share has actually remained relatively stable, growing by only a few percentage points over the past quarter-century. The data reveals the real drama of volatility among the mid-tier segment of service providers. While some have avoided a material drop in market share, Brown Brothers Harriman (BBH), long a standard-bearer for the mid-tier, slipped to tenth place in 2020 following a quantum leap in the client assets of CACEIS. While BBH's decline in our charts is exacerbated by a lack of updated reporting since mid-2021, it highlights a broader trend: in a market that prizes scale, the middle ground is becoming increasingly difficult to hold.

Northern Trust stands out as a rare success story in having achieved sustained growth in its market share over the years. By consistently outperforming its peers in service evaluations from sovereign wealth funds, other institutional investors and asset managers – as evidenced by ServiceMatrix data – the firm has significantly expanded its footprint.

The Era of Massive Consolidation

The early years of the millennium were defined by extensive merger and acquisition (M&A) activity that redrew the global map:

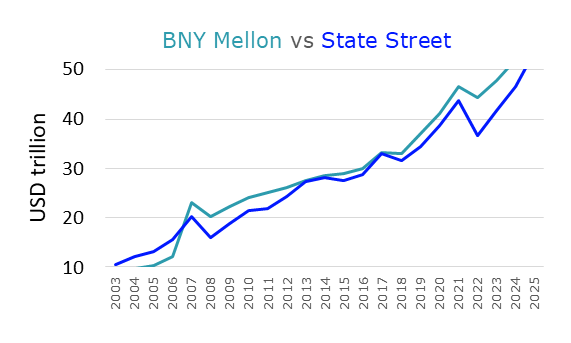

- The State Street Surge: In 2003, acquisition of Deutsche Bank's global custody business catapulted State Street from third place in the Assets under Custody (AUC) rankings to the top spot. Leapfrogging J.P. Morgan, the firm established a commanding lead over The Bank of New York, becoming the first firm to eclipse the $10 trillion AUC milestone.

- The Birth of a Titan: The 2007 merger of The Bank of New York and Mellon Group created BNY Mellon, reclaiming the throne. Since then, State Street has vied for the lead, coming within a whisker of its rival at year-end in 2013, 2014 and 2017, but BNY Mellon has outpaced the field since then.

- Secondary Waves: During this period, Citi expanded its footprint by acquiring BISYS Group (2007) and ING's local custody units (2013), BNY Mellon further fortified its position by absorbing BHF Asset Servicing GmbH (2010) and PNC Global Investor Services (2010) while State Street took over Investors Bank & Trust (2007) and Banca Intesa (2010).

Organic Growth and ‘Almost’ Mergers

Following this significant consolidation, the industry entered a quiet period in terms of wholesale acquisitions, with a peppering of M&A activity focused principally on expanding fund administration footprints and buying technology. For more than a decade now, growth in assets under custody has largely been organic, with the fastest-growing industry players winning more business (and losing fewer clients) than their rivals and, crucially, doing business with faster-growing asset owners and managers.

In the last five years, two potential deals would have shifted the market-share tectonic plates:

- State Street & BBH (2022): A proposed acquisition of Brown Brothers Harriman’s Investor Services division would have seen State Street overtake BNY Mellon for the number one spot. The deal’s collapse in late 2022 preserved the status quo but perhaps signalled a renewed appetite for consolidation.

- BNY Mellon & Northern Trust (2025): Recent reports of high-level discussions between the chief executives of these two top-five providers hinted at the prospect of a significant change, though an official offer has not materialized.

A service provider's headline figure for its client assets can refer purely to Assets under Custody or can extend to Assets under Custody and/or Administration. In some cases, it can include client assets for other lines of business, such as Corporate Trust/Issuer Services. The globalcustody.net data provides a 25-year longitudinal study which accounts for shifts in providers' calculation methodologies, restating historical data to ensure a like-for-like trend analysis. There’s more detail at About Assets under Custody.

Conclusion: A 25-Year Legacy of Scale

The evolution of global custody since 2000 is a story of consolidation and resilience. Over the last quarter-century, we have seen how a single strategic acquisition can redefine a firm's trajectory for a decade and how the loss of momentum can leave even the most storied players vulnerable. From the initial race to the milestone of $10 trillion of Assets under Custody to greater emphasis on service excellence, the data confirms two immutable truths: the giants have not only survived but become the very infrastructure of the global financial system, while select mid-tier players have grown their footprint considerably through superior service delivery to the most demanding, fast-growing asset owners and managers.

This site, like many others, uses small files called cookies to customize your experience. Cookies appear to be blocked on this browser. Please consider allowing cookies so that you can enjoy more content across assetman.net.

How do I enable cookies in my browser?

Internet Explorer

1. Click the Tools button (or press ALT and T on the keyboard), and then click Internet Options.

2. Click the Privacy tab

3. Move the slider away from 'Block all cookies' to a setting you're comfortable with.

Firefox

1. At the top of the Firefox window, click on the Tools menu and select Options...

2. Select the Privacy panel.

3. Set Firefox will: to Use custom settings for history.

4. Make sure Accept cookies from sites is selected.

Safari Browser

1. Click Safari icon in Menu Bar

2. Click Preferences (gear icon)

3. Click Security icon

4. Accept cookies: select Radio button "only from sites I visit"

Chrome

1. Click the menu icon to the right of the address bar (looks like 3 lines)

2. Click Settings

3. Click the "Show advanced settings" tab at the bottom

4. Click the "Content settings..." button in the Privacy section

5. At the top under Cookies make sure it is set to "Allow local data to be set (recommended)"

Opera

1. Click the red O button in the upper left hand corner

2. Select Settings -> Preferences

3. Select the Advanced Tab

4. Select Cookies in the list on the left side

5. Set it to "Accept cookies" or "Accept cookies only from the sites I visit"

6. Click OK

In the world of global custody and securities services, scale isn't just an advantage, it's the ultimate bedrock of survival for service providers. Both major and mid-tier players have grown considerably in terms of Assets under Custody – the quantum of their client assets – over the past 25 years.

Since the year 2000, globalcustody.net has been the go-to resource for Assets under Custody and Administration data for the world's leading providers of securities services. The data tells a definitive story of strategic acquisitions and 'near-miss' mergers, a journey from the first USD 10 trillion milestone to a modern era defined by technological arms races and service strength and consistency.

Shifting Sands in the Mid-Tier

While the dominance of the mega-custodians is undeniable, their collective market share has actually remained relatively stable, growing by only a few percentage points over the past quarter-century. The data reveals the real drama of volatility among the mid-tier segment of service providers. While some have avoided a material drop in market share, Brown Brothers Harriman (BBH), long a standard-bearer for the mid-tier, slipped to tenth place in 2020 following a quantum leap in the client assets of CACEIS. While BBH's decline in our charts is exacerbated by a lack of updated reporting since mid-2021, it highlights a broader trend: in a market that prizes scale, the middle ground is becoming increasingly difficult to hold.

Northern Trust stands out as a rare success story in having achieved sustained growth in its market share over the years. By consistently outperforming its peers in service evaluations from sovereign wealth funds, other institutional investors and asset managers – as evidenced by ServiceMatrix data – the firm has significantly expanded its footprint.

The Era of Massive Consolidation

The early years of the millennium were defined by extensive merger and acquisition (M&A) activity that redrew the global map:

- The State Street Surge: In 2003, acquisition of Deutsche Bank's global custody business catapulted State Street from third place in the Assets under Custody (AUC) rankings to the top spot. Leapfrogging J.P. Morgan, the firm established a commanding lead over The Bank of New York, becoming the first firm to eclipse the $10 trillion AUC milestone.

- The Birth of a Titan: The 2007 merger of The Bank of New York and Mellon Group created BNY Mellon, reclaiming the throne. Since then, State Street has vied for the lead, coming within a whisker of its rival at year-end in 2013, 2014 and 2017, but BNY Mellon has outpaced the field since then.

- Secondary Waves: During this period, Citi expanded its footprint by acquiring BISYS Group (2007) and ING's local custody units (2013), BNY Mellon further fortified its position by absorbing BHF Asset Servicing GmbH (2010) and PNC Global Investor Services (2010) while State Street took over Investors Bank & Trust (2007) and Banca Intesa (2010).

Organic Growth and ‘Almost’ Mergers

Following this significant consolidation, the industry entered a quiet period in terms of wholesale acquisitions, with a peppering of M&A activity focused principally on expanding fund administration footprints and buying technology. For more than a decade now, growth in assets under custody has largely been organic, with the fastest-growing industry players winning more business (and losing fewer clients) than their rivals and, crucially, doing business with faster-growing asset owners and managers.

In the last five years, two potential deals would have shifted the market-share tectonic plates:

- State Street & BBH (2022): A proposed acquisition of Brown Brothers Harriman’s Investor Services division would have seen State Street overtake BNY Mellon for the number one spot. The deal’s collapse in late 2022 preserved the status quo but perhaps signalled a renewed appetite for consolidation.

- BNY Mellon & Northern Trust (2025): Recent reports of high-level discussions between the chief executives of these two top-five providers hinted at the prospect of a significant change, though an official offer has not materialized.

A service provider's headline figure for its client assets can refer purely to Assets under Custody or can extend to Assets under Custody and/or Administration. In some cases, it can include client assets for other lines of business, such as Corporate Trust/Issuer Services. The globalcustody.net data provides a 25-year longitudinal study which accounts for shifts in providers' calculation methodologies, restating historical data to ensure a like-for-like trend analysis. There’s more detail at About Assets under Custody.

Conclusion: A 25-Year Legacy of Scale

The evolution of global custody since 2000 is a story of consolidation and resilience. Over the last quarter-century, we have seen how a single strategic acquisition can redefine a firm's trajectory for a decade and how the loss of momentum can leave even the most storied players vulnerable. From the initial race to the milestone of $10 trillion of Assets under Custody to greater emphasis on service excellence, the data confirms two immutable truths: the giants have not only survived but become the very infrastructure of the global financial system, while select mid-tier players have grown their footprint considerably through superior service delivery to the most demanding, fast-growing asset owners and managers.