From the desk of Roy Zimmerhansl

Practice lead, Pierpoint Financial Consulting

"Why should I lend my securities?" – I'm trying to think back to the first time I heard someone ask that question. It must have been in the early 1980s when I first became involved with the business. The simple answer then, as now is "to generate income from otherwise static portfolio holdings". If you consider that the pool of securities available for loan has grown to at least EUR 19.6 trillion, one could say "job done". Securities lending is an accepted practice in almost every country that has an established capital market. Indeed, index providers often require a market to include short selling and securities lending in order for it to be considered "developed".

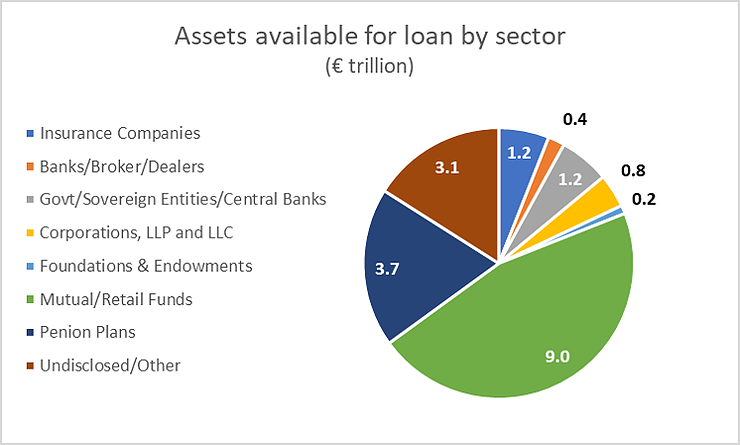

Investors that lend span the universe from retail investors via mutual funds, UCITS and ETFs through to central banks. The chart below draws on data provided in the most recent semi-annual ISLA Securities Lending Market Report using figures from IHS Markit and shows the total value of securities available for loan from each market segment. It clearly demonstrates the wide spectrum of investors participating in lending programmes and the incredible scale of their involvement.

Retail investors who lend benefit from increased fund performance or reduced costs for their funds.

Pension funds that lend accrue positive returns year after year, accumulating over time to make a meaningful contribution to portfolio performance. Sovereign Wealth Funds (SWFs) are huge investors that tend to outperform in this space, so it should come as no surprise that almost all the largest SWFs lend, adding significantly to their investment performance. Many central banks initially engaged only to avoid liquidity disruptions in secondary market trading but now are more active in generating returns for their massive portfolios accumulated over the past decade. I could go on, but I trust you get the picture.

The job isn't done for either markets or investors. In several active securities lending markets there isn't sufficient depth of supply beyond the primary index to facilitate trading. Further, not all markets allow short selling and securities lending yet, but the direction is clear and the absences few and far between (with, for example, the Nairobi Stock Exchange in the news most recently on the topic). Many notable investors in each category continue to abstain from lending, meaning the "Why" question hasn't been fully answered. I spend an inordinate amount of time thinking about this question and I have come up with five reasons which I will now explore further.

Suitability

Let me start by recognising that lending isn't for everyone. There is a certain asset size required in order to be able to generate returns, while not all assets have borrowing demand. Additionally, it can be a valid concern for managers of small cap funds as they could have disproportionately large holdings in small companies and are concerned about supply/demand imbalances.

Bottom line: Securities lending is appropriate for most but not all institutional investors.

Ethics

In my experience, non-participants are less concerned about the ethics of securities lending per se, rather they focus on short sellers. "Why should I lend my securities to a short seller?" is a commonly asked question by non-lenders. I recommend that people read Are short sellers ethical? by Duncan Lamont of Schroders, which covers various short selling motivations. Let me add two comments to Mr. Lamont's overview.

1. Short sellers do not have magic dust. Where shorting for a directional trade, they are expressing a negative view on the company in the same way as a holder of the same stock has a different view. Over time, stocks have risen so there is an inherent bias against the short seller. And remember that every time an investor buys a stock, they are already expressing an opposite opinion to the seller (which may or may not be a short seller) and only time will prove which view is correct.

2. Regulators have recognised the value short selling brings to price discovery, market liquidity and its smoothing effect on market peaks and troughs. That is unlikely to change except for temporary periods that are scenario specific. Short selling dates back to the early 1600s and isn't going away.

Bottom line: Ultimately, I think it unlikely that any argument from a securities lending advocate will change anyone's opinion on the ethics of short selling being the prerequisite for the demand for securities lending.

Risk

As with all investment activity, securities lending carries risk. The two primary risks are counterparty default and cash collateral reinvestment losses. The Lehman Brothers default provides a real example of the impact of the largest securities-borrower default in history.

Losses from securities lending are few and far between due to the collateralised nature of the business and indemnifications provided by agent lenders. Forced sales of assets purchased with cash collateral did cause losses which were exacerbated by the Lehman default, but the market conditions leading to those losses started gathering momentum a year earlier when the sub-prime market started to impact money markets and investments.

Critically, it is investors that determine how aggressive their reinvestment policy is, and of course, most have the option of accepting only non-cash collateral and avoiding reinvestment risk altogether. Adam McCullough of Morningstar provides a useful examination of securities lending risk and reward that you can read here.

Bottom line: Securities lending is a positive contributor to revenues in rising or falling markets. History has demonstrated that it is a low-risk, relatively low-return business that adds cumulative performance year after year.

Differentiator

I have come across product managers who differentiate themselves from competitors by promoting the fact that they do not lend. That is a valid position to take, but investors in those products should be cognisant of the likely underperformance or higher operating costs vis-à-vis products that lend. In the end, investors will vote with their cash, so if it is an important differentiator, then those funds will accumulate assets faster.

Bottom line: I have yet to see that lending abstinence has had any meaningful impact in gathering assets from investors.

Knowledge

Over the years, securities lending education from service providers and outside observers has improved dramatically.

Yet there is still a gap and many investors that could benefit substantially from lending remain outside the business. It may be that these investors have taken an informed decision not to engage in lending and the matter has ended there. However, in our experience, it is also true that many non-lenders have questions which have not been answered satisfactorily and comprehensively or that investors remain unclear or sceptical.

That's where Pierpoint Financial Consulting comes in, with the firm's Insights on Securities Lending for Non-Lenders and Trustees. This free product provides bespoke information, guidance and views for non-lenders and independent trustees, delivered by an unbiased, independent team of experts with years of leadership experience in securities lending.

Bottom line: I am encouraged by the tremendous growth in the intervening 35+ years since someone first asked me "Why should I lend my securities" but recognise that there is still work to do.

This site, like many others, uses small files called cookies to customize your experience. Cookies appear to be blocked on this browser. Please consider allowing cookies so that you can enjoy more content across assetman.net.

How do I enable cookies in my browser?

Internet Explorer

1. Click the Tools button (or press ALT and T on the keyboard), and then click Internet Options.

2. Click the Privacy tab

3. Move the slider away from 'Block all cookies' to a setting you're comfortable with.

Firefox

1. At the top of the Firefox window, click on the Tools menu and select Options...

2. Select the Privacy panel.

3. Set Firefox will: to Use custom settings for history.

4. Make sure Accept cookies from sites is selected.

Safari Browser

1. Click Safari icon in Menu Bar

2. Click Preferences (gear icon)

3. Click Security icon

4. Accept cookies: select Radio button "only from sites I visit"

Chrome

1. Click the menu icon to the right of the address bar (looks like 3 lines)

2. Click Settings

3. Click the "Show advanced settings" tab at the bottom

4. Click the "Content settings..." button in the Privacy section

5. At the top under Cookies make sure it is set to "Allow local data to be set (recommended)"

Opera

1. Click the red O button in the upper left hand corner

2. Select Settings -> Preferences

3. Select the Advanced Tab

4. Select Cookies in the list on the left side

5. Set it to "Accept cookies" or "Accept cookies only from the sites I visit"

6. Click OK

From the desk of Roy Zimmerhansl

Practice lead, Pierpoint Financial Consulting

"Why should I lend my securities?" – I'm trying to think back to the first time I heard someone ask that question. It must have been in the early 1980s when I first became involved with the business. The simple answer then, as now is "to generate income from otherwise static portfolio holdings". If you consider that the pool of securities available for loan has grown to at least EUR 19.6 trillion, one could say "job done". Securities lending is an accepted practice in almost every country that has an established capital market. Indeed, index providers often require a market to include short selling and securities lending in order for it to be considered "developed".

Investors that lend span the universe from retail investors via mutual funds, UCITS and ETFs through to central banks. The chart below draws on data provided in the most recent semi-annual ISLA Securities Lending Market Report using figures from IHS Markit and shows the total value of securities available for loan from each market segment. It clearly demonstrates the wide spectrum of investors participating in lending programmes and the incredible scale of their involvement.

Retail investors who lend benefit from increased fund performance or reduced costs for their funds.

Pension funds that lend accrue positive returns year after year, accumulating over time to make a meaningful contribution to portfolio performance. Sovereign Wealth Funds (SWFs) are huge investors that tend to outperform in this space, so it should come as no surprise that almost all the largest SWFs lend, adding significantly to their investment performance. Many central banks initially engaged only to avoid liquidity disruptions in secondary market trading but now are more active in generating returns for their massive portfolios accumulated over the past decade. I could go on, but I trust you get the picture.

The job isn't done for either markets or investors. In several active securities lending markets there isn't sufficient depth of supply beyond the primary index to facilitate trading. Further, not all markets allow short selling and securities lending yet, but the direction is clear and the absences few and far between (with, for example, the Nairobi Stock Exchange in the news most recently on the topic). Many notable investors in each category continue to abstain from lending, meaning the "Why" question hasn't been fully answered. I spend an inordinate amount of time thinking about this question and I have come up with five reasons which I will now explore further.

Suitability

Let me start by recognising that lending isn't for everyone. There is a certain asset size required in order to be able to generate returns, while not all assets have borrowing demand. Additionally, it can be a valid concern for managers of small cap funds as they could have disproportionately large holdings in small companies and are concerned about supply/demand imbalances.

Bottom line: Securities lending is appropriate for most but not all institutional investors.

Ethics

In my experience, non-participants are less concerned about the ethics of securities lending per se, rather they focus on short sellers. "Why should I lend my securities to a short seller?" is a commonly asked question by non-lenders. I recommend that people read Are short sellers ethical? by Duncan Lamont of Schroders, which covers various short selling motivations. Let me add two comments to Mr. Lamont's overview.

1. Short sellers do not have magic dust. Where shorting for a directional trade, they are expressing a negative view on the company in the same way as a holder of the same stock has a different view. Over time, stocks have risen so there is an inherent bias against the short seller. And remember that every time an investor buys a stock, they are already expressing an opposite opinion to the seller (which may or may not be a short seller) and only time will prove which view is correct.

2. Regulators have recognised the value short selling brings to price discovery, market liquidity and its smoothing effect on market peaks and troughs. That is unlikely to change except for temporary periods that are scenario specific. Short selling dates back to the early 1600s and isn't going away.

Bottom line: Ultimately, I think it unlikely that any argument from a securities lending advocate will change anyone's opinion on the ethics of short selling being the prerequisite for the demand for securities lending.

Risk

As with all investment activity, securities lending carries risk. The two primary risks are counterparty default and cash collateral reinvestment losses. The Lehman Brothers default provides a real example of the impact of the largest securities-borrower default in history.

Losses from securities lending are few and far between due to the collateralised nature of the business and indemnifications provided by agent lenders. Forced sales of assets purchased with cash collateral did cause losses which were exacerbated by the Lehman default, but the market conditions leading to those losses started gathering momentum a year earlier when the sub-prime market started to impact money markets and investments.

Critically, it is investors that determine how aggressive their reinvestment policy is, and of course, most have the option of accepting only non-cash collateral and avoiding reinvestment risk altogether. Adam McCullough of Morningstar provides a useful examination of securities lending risk and reward that you can read here.

Bottom line: Securities lending is a positive contributor to revenues in rising or falling markets. History has demonstrated that it is a low-risk, relatively low-return business that adds cumulative performance year after year.

Differentiator

I have come across product managers who differentiate themselves from competitors by promoting the fact that they do not lend. That is a valid position to take, but investors in those products should be cognisant of the likely underperformance or higher operating costs vis-à-vis products that lend. In the end, investors will vote with their cash, so if it is an important differentiator, then those funds will accumulate assets faster.

Bottom line: I have yet to see that lending abstinence has had any meaningful impact in gathering assets from investors.

Knowledge

Over the years, securities lending education from service providers and outside observers has improved dramatically.

Yet there is still a gap and many investors that could benefit substantially from lending remain outside the business. It may be that these investors have taken an informed decision not to engage in lending and the matter has ended there. However, in our experience, it is also true that many non-lenders have questions which have not been answered satisfactorily and comprehensively or that investors remain unclear or sceptical.

That's where Pierpoint Financial Consulting comes in, with the firm's Insights on Securities Lending for Non-Lenders and Trustees. This free product provides bespoke information, guidance and views for non-lenders and independent trustees, delivered by an unbiased, independent team of experts with years of leadership experience in securities lending.

Bottom line: I am encouraged by the tremendous growth in the intervening 35+ years since someone first asked me "Why should I lend my securities" but recognise that there is still work to do.